Canada Departure Tax 101 What Happens When You Try to Leave

This is educational, not individualized tax advice. Consult a qualified professional before restructuring. If you would like to work with us, reach out via DM on X @BowtiedBrazil

You’re thinking about joining the great Canadian exit parade.

The airport line feels longer every month and if you believe social media half the country is pushing a luggage cart toward Portugal, Dubai, or even the US (you should believe social media because our Canadian business is on fire right now with people leaving).

Before you collect passport stamps, the Canada Revenue Agency wants one more conversation about money: the departure tax.

The departure tax treats much of what you own as if you sold it the night before you become a nonresident (even if you don’t). Every unrealised gain you built while living in Canada shows up on one last return

Residency rules in plain language

Canada taxes worldwide income only while it considers you resident and residency is measured by ties not by your passport. A dwelling that stays available a spouse or partner remaining in Canada or children in local school are primary ties. Secondary ties range from provincial health coverage and driver licences to bank accounts memberships and even your Netflix billed to a Canadian card. Cut the primary ties first then whittle the secondary list. When the strongest link left is a tinder profile with passport mode on in Montreal you’re prob good

The deemed disposition: what really happens

At 11:59 pm the night before you break residency, CRA conducts a paper only auction of almost everything you own. It assumes you dispose of each listed asset at fair market value and immediately buy it back for the same amount. The difference between your historical cost and that fair value is a capital gain or loss. Half of that gain becomes taxable income at your marginal rate. (This is called deemed disposition and basically is a capital gains tax even if there was no sale)

Because it is pretend, you receive zero cash yet you may owe real tax. CRA allows you to defer payment by filing Form T1244 and providing security for any tax above about $25k (CAD)(. Interest is suspended while the security stands so a properly documented deferral keeps cash in your pocket until you actually sell the asset

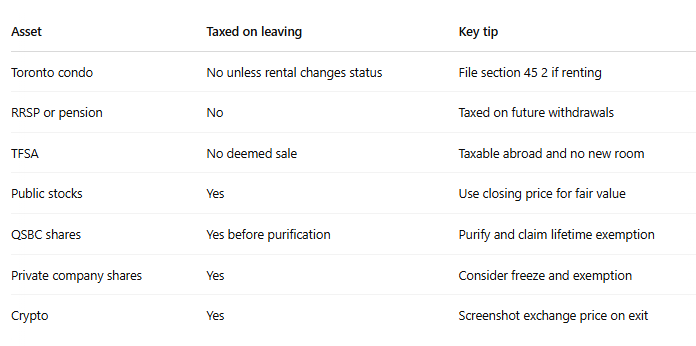

What gets hit what gets a pass

Public company shares, crypto, foreign rental properties, partnership units, and many overseas pensions all get taxed. Canadian real estate is exempt until the day you really do sell. RRSP, RRIF, and other registered pensions remain tax sheltered here and only trigger withholding when you draw them.

TFSAs keep their Canadian tax free status but most countries will tax future income and you stop adding new room the moment you leave. Assets used in an active Canadian business escape the deemed sale as long as the business continues

QSBC shares and the lifetime exemption

Founders holding qualifying small business corporation shares can shelter up to about $1mm (CAD) of gains under the lifetime capital gains exemption (LGCE).

To use it, the corporation must be a Canadian controlled private corporation (CCPC) with at least 90% of its assets used in an active Canadian business at the moment of sale.

If excess cash or passive investments muddy that ratio, you can do what’s called a purification before departure by paying dividends or moving surplus assets to a holdco. Claim the exemption on your final return and the sheltered portion sidesteps the goodbye tax entirely. The hardest part of qualifying is meeting the active asset tests so seek out guidance on that.

Private company shares freeze tricks

Deferring tax on private company shares can trigger a tax rule that recharacterises capital gains as dividends. Many founders implement a freeze before they leave. They exchange their common shares for fixed value preferred shares and thereby crystallise today’s gain possibly using the lifetime exemption then allow new common shares owned by a foreign entity to capture future growth outside Canada. (don’t do this on your own lol)

Structuring that stays legal and still helps

Rolling high gain assets into a Canadian holdco before exit leaves you with a smaller personal gain today and only withholding tax on future dividends. Moving shares into a treaty country corporation can avoid the goodbye tax altogether when done with genuine substance clear valuations and a signed section 85 rollover. Intercompany loans at arm’s length interest and short term management fee arrangements can also migrate cash efficiently once you are nonresident. The common thread is paperwork first substance always and tax rates second

Cancel provincial health coverage, swap your driver licences, close Canadian credit cards, and even streaming services linked to domestic payment methods. Auditors read digital breadcrumbs when deciding if you truly left

If you have a company/business, seek out professional guidance as soon as you begin to consider leaving- the more time you have pre-move, the more options we have to work with to reduce or eliminate this tax